What is the Personal Savings Allowance? Information about tax on savings interest

A Personal Savings Allowance, sometimes shortened to PSA, is the amount of interest you can earn before you have to start paying tax - this is based on your income tax band. From 6th April 2016 banks and building societies no longer automatically deduct tax from savings. While both basic and higher rate taxpayers will be entitled to the Personal Savings Allowance, the maximum amount will depend on your earnings. Get more information at HMRC Personal Savings Allowance factsheet.

For other tax band information, please visit Gov.uk.

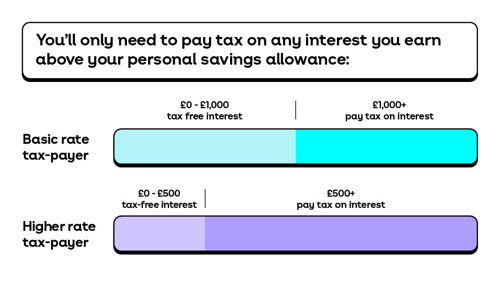

If you are a basic-rate taxpayer up to £1,000 of your savings income will be tax-free (£500 for higher rate taxpayers).

The table below shows how much you’d need in a standard savings account to hit the basic-rate taxpayers Personal Savings Allowance:

| Interest rate | Basic-rate taxpayer |

| 1.00% | £99,997 |

| 2.00% | £49,997 |

This table is for illustrative purposes only and assumes a lump sum deposit with no withdrawals or further deposits. Interest has been calculated daily and it is based on an annual interest rate.

From 6th April 2016, building societies and banks stopped applying tax to savings interest. It is your responsibility to declare any interest you earn over your personal savings allowance directly to HMRC.

Savings income is any interest earned from the following:

- Bank and building society accounts.

- Savings and credit union accounts.

- Unit trusts, investment trusts and open-ended investment companies.

- Peer-to-peer lending.

- Trust funds.

- Payment protection insurance (PPI).

Your allowance also applies to interest from:

- Government or company bonds.

- Life annuity payments.

- Some life insurance contracts.

If you have a joint account the interest is split equally between the account holders and then treated individually depending on your personal tax circumstances.

No. As interest from ISAs is tax free it will not count towards your Personal Savings Allowance.

No. You don’t have to divulge anything about your tax status or savings income to any account providers.

The answer is a simple yes. For many people, ISAs are still an attractive way to save.

For most people it will still be best to put their money into a top cash ISA first, and then use the Personal Savings Allowance after that.

The most important thing is that in an ISA your money is protected from tax year after year, so even if the Government changes the rules again you will be protected.

Also, your personal circumstances might change. With your money in an ISA, even if your income goes into the higher tax band you’ll still earn tax-free interest.

Interest rates might go up and this would change the amount you could save before being taxed.