Tax-free savings

An ISA, or Individual Savings Account, is a super handy way to save and invest your money here in the UK. Think of it like a special wrapper for your savings and investments, helping them grow without UK Income Tax or Capital Gains Tax getting in the way. You get to keep more of your money - how good is that?!

Every tax year (that runs from April 6th to April 5th), the government gives us all an ISA allowance. This is the most you can pop into all your ISAs that year. Right now, for adults, that's £20,000. You can put all of that into one type of ISA, or spread it across a few, as long as you don't go over your total allowance. It's all about making your money work harder for you, tax-efficiently.

Here are the different types of ISAs you can find in the UK. Each one is a bit different, so you can pick the one that fits your money goals and how much risk you're comfortable with:

Cash ISA

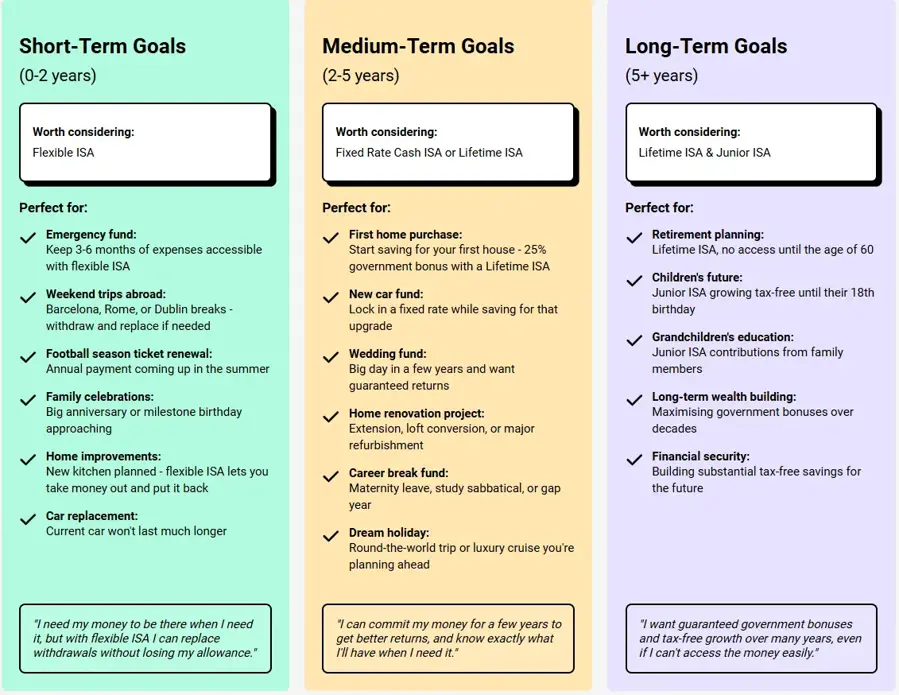

This one's pretty straightforward - it's a tax-free savings account. You pop your cash in, and any interest you earn is all yours, tax-free. Cash ISAs are great for short, medium and long-term savings goals or if you just prefer to play it safe. You can usually find both easy-access and fixed-rate options.

Stocks and shares ISA

If you're looking to invest, this is your go-to. It lets you put your money into things like company shares, funds, or bonds, all wrapped up tax-free. While there's a chance for bigger returns than a cash ISA, remember that the value of investments can go up or down, so your money is at risk.

Lifetime ISA (LISA)

This one's specifically for our members aged 18 to 39. A LISA can be a real help if you're saving up for your first home or for your retirement. You can save up to £4,000 each tax year, and the government even adds a lovely 25% bonus to your contributions.

Innovative Finance ISA

With an Innovative finance ISA, you can lend money to other people or businesses through special online platforms (this is called peer-to-peer lending) and earn tax-free interest. These can sometimes offer higher returns than Cash ISAs, but they do come with higher risks, and your money might not be protected by the FSCS.

At Nottingham Building Society we don't offer stocks and shares or innovative finance ISAs, but you can open these alongside our cash ISAs with other providers. However please be mindful that your payments into these ISAs will contribute towards your £20,000 annual ISA allowance.

- Must be 18 or over to open an ISA (If you’re opening a Lifetime ISA you must also be under 40).

- Must be a UK resident for tax purposes.

- You can only pay into one cash ISA per tax year with us.

- ISA allowance: £20,000 (current tax year).

- Lifetime ISA limit: £4,000 per tax year.

- Junior ISA allowance: £9,000 per tax year.

For the current tax year, you can save up to £20,000 across all your ISAs. This is referred to as an ISA allowance.

-

- Cash ISA

- Stocks and shares ISA

- Lifetime ISA

- Innovative ISA

- If you have a Lifetime ISA, the maximum amount you can put in is £4,000 per tax year (this counts towards your £20,000 total allowance).

- Your ISA allowance for a Junior ISA is £9,000, but this is separate and does not contribute to your adult ISA allowance of £20,000.

You can split your ISA allowance

You can split your ISA allowance across the 4 ISA types, for example:

Option 1: £20,000 all in one cash ISA.

Option 2: £4,000 Lifetime ISA + £16,000 cash ISA (e.g. fixed rate ISA).

Option 3: £10,000 cash ISA + £10,000 stocks & shares ISA.

Use it or lose it

ISA allowances reset on 6 April each year. Any unused allowance from the previous tax year cannot be carried forward into the next tax year.

but you can transfer money between ISA providers without it affecting your annual allowance.