What's a repayment mortgage?

A repayment mortgage (sometimes called a capital and interest mortgage) is where your monthly payment covers two things: part of the amount you originally borrowed (the capital) and the interest your lender charges on top.

With every payment you make, the amount you owe gets a little smaller. Keep up your payments for the full term and the mortgage is completely paid off. You own the property outright.

This is different from an interest-only mortgage, where your monthly payments only cover the interest. With interest-only, you still owe the full amount at the end and need a plan to pay it back in one go.

| Repayment mortgages are by far the most popular choice for homebuyers in the UK. If you’re buying a home to live in, this is almost certainly the type of mortgage you’ll be offered. |

How does a repayment mortgage work?

Your lender works out a monthly payment amount that, if you pay it every month for the full mortgage term, will clear the whole debt, capital and interest.

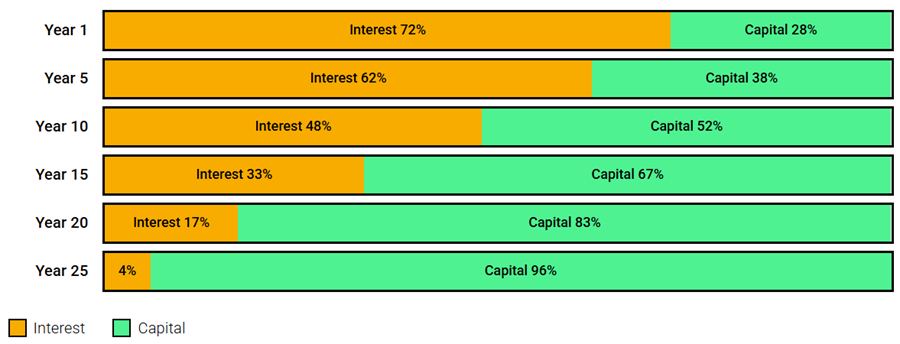

Here’s the part that catches some people off guard: in the early years, most of your monthly payment goes towards interest, not the capital. As time goes on, the balance tips. You’ll be paying less in interest and more towards actually owning your home.

This happens because interest is calculated on the outstanding balance. When you owe more, you pay more interest. As the balance drops, so does the interest charge, and more of your payment chips away at the capital.

How your monthly payment splits over time

Based on a 25-year repayment mortgage. Each row shows the same monthly payment, but the split between interest and capital changes.

This is why your annual mortgage statement might feel a bit deflating in the first few years. It can look like the amount you owe hasn’t budged much. Don’t worry. It’s working as it should. The pace picks up as you go.

Work out your monthly repayments

Knowing the theory is useful, but seeing actual numbers makes it real. Use our mortgage repayment calculator to get an estimate based on the amount you want to borrow, your interest rate and your preferred term.

You can try different scenarios to see how changing the deposit size, term length or interest rate affects what you’d pay each month.